If you’re considering a payday loan to manage immediate expenses while looking into Propecia for hair loss, understanding both options is vital. Payday loans offer quick access to cash, usually with minimal paperwork. These loans can help bridge the gap in your finances, but they often come with high interest rates. Always calculate the total repayment amount before committing.

Propecia, a popular treatment for male pattern baldness, requires careful evaluation too. Consult with a healthcare provider to ensure it’s the right choice for you. While it may help with hair regrowth, it can have side effects that warrant attention. Balance your financial decisions with your health needs for the best outcome.

When you’re ready to move forward with a payday loan, look for reputable online lenders. Check reviews, compare terms, and ensure they comply with regulatory standards. For Propecia, order medication from licensed pharmacies to avoid counterfeit products and receive genuine treatment. Prioritize safety and informed choices in both financial and health matters for peace of mind.

- Payday Loans Online and Propecia: A Comprehensive Guide

- Understanding Payday Loans

- Managing Propecia Costs

- Understanding Payday Loans: What You Need to Know

- How to Apply for Payday Loans Online Safely

- Propecia Overview: Uses and Benefits

- The Connection Between Payday Loans and Medical Expenses

- Evaluating the Costs of Payday Loans for Propecia Purchases

- Interest and Fees Breakdown

- Alternatives to Payday Loans

- Alternatives to Payday Loans for Funding Propecia

- Legal Considerations for Payday Loans Online

- Tips for Managing Debt from Payday Loans

- Create a Budget

- Consider Consolidation Options

Payday Loans Online and Propecia: A Comprehensive Guide

Consider exploring payday loans online if you’re looking for quick funding to cover unexpected expenses associated with Propecia treatments. These loans typically offer fast approval, allowing you to address your financial needs without delay.

Understanding Payday Loans

Payday loans are short-term solutions designed to help individuals bridge the gap between paychecks. Here’s what you need to know:

- Quick Access: Funds usually transfer to your bank account within one business day.

- Application Process: The online application is simple, often requiring basic personal and financial information.

- Repayment Terms: Typically due on your next payday, but options for extension may be available.

- Interest Rates: Be aware that interest rates can be significantly higher than traditional loans.

Managing Propecia Costs

Propecia, while effective for treating hair loss, can be an added expense. Here are strategies to manage those costs alongside potential payday loans:

- Insurance Coverage: Check if your insurance plan offers any reimbursement for Propecia.

- Generic Options: Talk to your healthcare provider about generic versions that may be more affordable.

- Shipping Discounts: Some online pharmacies offer reduced rates for subscriptions or bulk orders.

Knowing how payday loans can aid in financing your treatment will enable you to navigate your options wisely. Always read the loan terms thoroughly and ensure you can meet repayment requirements to avoid financial strain.

Understanding Payday Loans: What You Need to Know

Payday loans offer quick access to cash, typically for individuals facing short-term financial needs. These loans usually have a high-interest rate and are often due on the borrower’s next payday. Consider careful planning before applying, as repayment can lead to financial strain if you do not manage your expenses effectively.

Loan Amounts and Terms: Most payday loans range from $100 to $1,000. Terms vary, but repayment usually occurs within two to four weeks. Read the contract carefully to understand the interest rate and any additional fees that apply, as these can significantly increase the total cost of the loan.

Interest Rates: Be aware that payday loans can have annual percentage rates (APRs) that exceed 400%. This can make them an expensive option compared to other forms of credit. Before borrowing, compare your options with personal loans or credit cards to find more favorable terms.

Application Process: The application process for payday loans is typically straightforward and can be completed online. Lenders usually require minimal documentation, such as proof of income and identification. This ease of access can appeal to those needing immediate funds.

Potential Risks: Borrowers often struggle with repayment because of the high costs associated with these loans. Late fees and increased interest rates can lead to a cycle of debt. If you find yourself unable to repay, communicate with your lender to discuss options, as they may offer extensions or payment plans.

Alternatives: Investigate alternatives before committing to a payday loan. Options include asking friends or family for assistance, negotiating bills, or seeking assistance from local charities. Credit unions may offer small, low-interest loans that can provide relief without the burden of high fees.

Understanding the implications of payday loans ensures you make informed decisions. Assess your financial situation, explore all available options, and choose wisely to maintain your financial health.

How to Apply for Payday Loans Online Safely

Choose a reputable lender. Research online reviews and verify the company’s credentials before proceeding with an application. Look for lenders that are transparent about their fees and terms.

Review the loan agreement carefully. Focus on the interest rates, repayment terms, and any hidden charges. Ensure you understand your obligations to avoid surprises later.

Provide accurate and honest information. When filling out your application, enter your personal details, income, and expenditure truthfully. This prevents potential issues with loan approval and repayment.

Secure your personal information. Use websites with HTTPS in their URLs to ensure your data is encrypted. Avoid using public Wi-Fi for financial transactions to protect your sensitive information.

Consider your repayment strategy. Before taking a loan, evaluate your budget to determine how you will repay it without compromising your financial stability. Set reminders for payment due dates to avoid late fees.

Reach out to customer support. If any aspect of the loan process is unclear, don’t hesitate to ask questions. Good lenders will provide assistance and clarification when needed.

Be cautious with multiple applications. Applying for several loans at once can negatively affect your credit score. Limit applications to one or two lenders and wait for approval before applying elsewhere.

Look for alternatives if you have concerns. Sometimes, payday loans may not be the best option. Explore other financial solutions such as credit unions or personal loans with better terms.

Propecia Overview: Uses and Benefits

Propecia, containing finasteride, primarily treats male pattern baldness. It effectively diminishes hair loss, promotes regrowth, and is FDA-approved for this purpose.

Key uses of Propecia include:

- Restoration of hair in men experiencing thinning or receding hairlines.

- Improvement of hair density on the scalp.

- Maintenance of existing hair by inhibiting hormone conversion linked to hair loss.

The benefits of Propecia extend beyond mere aesthetics:

- Many users report increased self-confidence as hair density improves.

- Propecia offers a non-invasive option compared to hair transplant surgeries.

- Research shows that many users experience noticeable results within three to six months of consistent use.

While Propecia is effective, discussing potential side effects with a healthcare provider is advisable. Side effects may include decreased libido and erectile dysfunction, although these are not common.

In sum, Propecia serves as a practical solution for men confronting hair loss, offering tangible benefits in hair restoration and self-esteem enhancement.

The Connection Between Payday Loans and Medical Expenses

Consider using payday loans to manage unexpected medical expenses. These short-term loans provide quick cash access, which can be critical in emergencies. Medical bills often arise suddenly, and not everyone has savings to cover them. In such cases, payday loans can bridge the gap, allowing you to pay for necessary treatments without delay.

Statistics show that medical expenses contribute significantly to personal debt. A survey indicated that nearly 67% of bankruptcies in the U.S. are tied to medical costs. When faced with high deductibles or out-of-pocket expenses, many individuals turn to payday loans, prioritizing immediate healthcare over long-term financial implications.

Researching lenders is essential before opting for a payday loan. Look for reputable companies that offer transparent terms and fair interest rates. Understand the repayment schedule, as failing to repay on time can lead to a cycle of debt that complicates financial recovery.

Explore other financing options as well. Consider health credit cards or medical payment plans offered by some healthcare providers. These alternatives might provide lower interest rates compared to payday loans and are often designed for medical expenses specifically.

Planning for future medical costs can also alleviate the need for payday loans. Regular savings for healthcare emergencies can reduce financial stress and reliance on high-interest borrowing. Utilize budgeting tools to ensure you set aside funds for unexpected bills.

In summary, payday loans offer a solution for urgent medical expenses, but they should be approached with caution. Always weigh the pros and cons, and consider alternative financing options to avoid long-term financial strain.

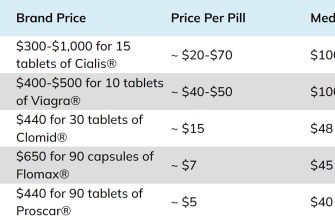

Evaluating the Costs of Payday Loans for Propecia Purchases

Before opting for a payday loan to buy Propecia, calculate the total costs carefully. Payday loans typically come with high fees, often ranging from $15 to $30 per $100 borrowed, translating to an annual percentage rate (APR) that can exceed 400%. This means that a $500 loan could cost you between $575 and $650 if paid back within two weeks.

Interest and Fees Breakdown

Analyze the repayment terms of any payday loan. If you take a loan for $300 with a $45 fee and repay it in two weeks, you will owe $345. Failing to repay on time leads to rollovers, which escalate fees quickly, compounding the debt. Always check the lender’s policy on renewals and late payments.

Alternatives to Payday Loans

Consider alternatives like credit union loans or personal loans from a bank. These options often have lower interest rates and better terms. Some pharmacies offer payment plans, allowing for more manageable payments. Research these options before committing to a payday loan for Propecia purchases.

Alternatives to Payday Loans for Funding Propecia

Consider using a health savings account (HSA) if eligible. HSAs allow you to save money tax-free for medical expenses, including prescriptions like Propecia. This option not only provides funds without interest but also supports long-term health savings.

Credit unions often offer lower-interest personal loans compared to payday lenders. Joining a local credit union can lead to better rates and more favorable terms for borrowing, making them a solid choice for funding Propecia.

Look into medical financing options specifically designed for healthcare costs. Several companies offer loans or payment plans that cater to prescription medications. These plans typically come with lower interest rates than payday loans, making them easier to repay.

Consider negotiating with your healthcare provider. Some clinics may offer payment plans that allow for installments without high-interest rates. This option keeps the costs manageable while ensuring you have access to Propecia when needed.

Explore government assistance programs. Some states provide support for medication costs, especially for those with specific financial constraints. Researching available programs may yield options that reduce or eliminate the need for loans.

Utilize family or friends for short-term loans. Borrowing from people you trust can save you from high-interest borrowing options. Make sure to establish clear terms to maintain positive relationships.

Legal Considerations for Payday Loans Online

Understand your rights as a borrower before engaging in online payday loans. Most states impose regulations that limit the interest rates lenders can charge. Check your state’s laws to know the maximum allowed rates and fees.

Make sure to read the loan agreement thoroughly. This document outlines all terms, including repayment schedules, interest rates, and any additional fees. Ensure you understand each component before signing.

Be aware of the consequences of defaulting on a payday loan. Many lenders can pursue legal action to recover unpaid amounts. Laws vary by state, but repercussions may include wage garnishment or negative impacts on credit scores.

Look for licensed lenders operating in your state. Each state has specific licensing requirements for payday loan providers, ensuring they follow legal practices. Verify this information on your state’s financial regulatory website.

If you encounter unethical practices or feel pressured, report the lender to your state’s regulatory agency. Consumer protection agencies monitor complaints and can take action against lenders who violate laws.

Consider alternatives to payday loans. Local credit unions or community banks often offer short-term loans with better terms. Explore these options to avoid high-interest rates associated with payday lending.

Tips for Managing Debt from Payday Loans

Prioritize your payments. Focus on settling high-interest debts first to minimize total interest paid over time. Create a list of all your debts, including amounts owed and interest rates. This helps you visualize your financial commitments and strategize effectively.

Create a Budget

A budget outlines your income and expenses, giving you a clear picture of your finances. Allocate specific amounts for essential expenses like housing and groceries, then designate a portion for debt repayment. Regularly review and adjust your budget to ensure you stay on track.

Consider Consolidation Options

Look into debt consolidation to combine multiple payday loans into one single loan, often with a lower interest rate. This simplifies repayment and can potentially reduce the total amount paid monthly. Research reputable lenders or credit unions that offer consolidation plans.

| Action | Benefits |

|---|---|

| Prioritize Payments | Reduces overall interest costs |

| Create a Budget | Provides a clear financial overview |

| Debt Consolidation | Simplifies repayments and lowers interest |

| Negotiate with Lenders | Possibility of lower interest rates or payment plans |

Negotiate with lenders to discuss possible extensions on payment deadlines or lower interest rates. Open communication can lead to favorable modifications, easing your repayment process.

Seek professional advice if you’re facing overwhelming debt. Financial advisors or credit counselors can provide personalized strategies and resources tailored to your needs.